Mortgage Rate Switch & Product Transfer

Independent product transfer advice from a family-run Chorley broker. We review your options across Lancashire, Greater Manchester and nationwide, and for a straightforward rate switch, we don't charge a client fee.

Live Mortgage Rates

No credit check

Live rates from 90+ lenders

Takes less than 2 minutes

No contact details required for results

Free credit report when you enquire with us

Advice by phone, video or in our Chorley offices

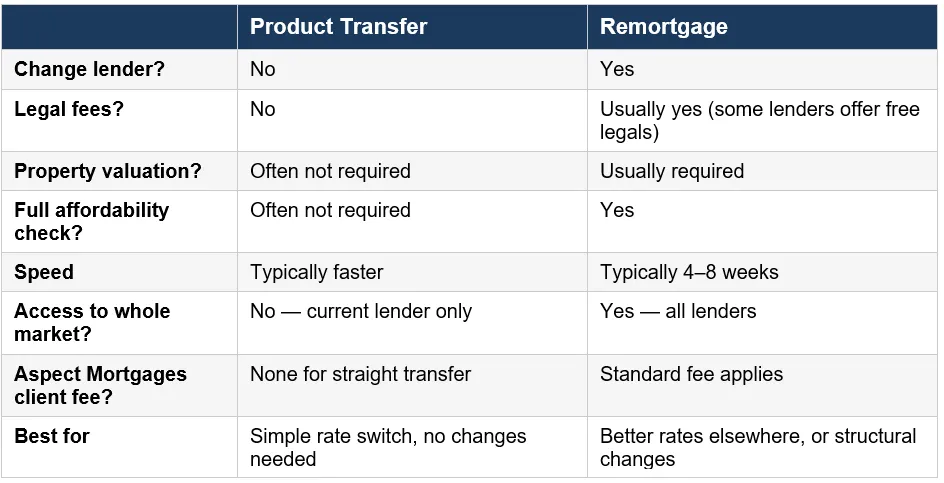

What Is a Mortgage Product Transfer (Rate Switch)?

A product transfer - or rate switch, as most people call it - is when you move from your existing mortgage deal (such as a fixed or tracker rate) onto a new deal with the same lender, once your current one expires.

Unlike a full remortgage, a product transfer doesn't involve switching lenders. That means:

No solicitor or legal fees

No full property valuation in most cases

No affordability reassessment in many cases

A faster, simpler process from start to finish

For many homeowners, particularly those in unstable financial circumstances or with limited equity, a product transfer can be the most practical and cost-efficient option. But it's not automatically the right choice, which is why it's worth speaking to an advisor about your options.

When Should You Start the Process?

The short answer: earlier than you think. Most lenders allow you to reserve a new product rate around 3 months before your current deal ends, with the new rate activating automatically when the old one expires.

This matters because:

If rates rise before your deal ends, you'll be protected at the rate you locked in.

If rates fall before your deal completes, many lenders allow you to switch to a lower rate - though this varies by lender.

You avoid rolling onto the SVR, which is almost always significantly higher than any fixed or tracker deal.

If your new rate is lower, many lenders will allow you to start the new deal early, without exit fees. This can mean a few months on a lower rate than the one you are currently locked in to.

We recommend getting in touch around four months before your current deal ends. That gives us plenty of time to review your options, make a recommendation, and arrange everything at your pace without any last-minute pressure.

What If You Want To Make Changes At The Same Time?

Sometimes a product transfer is also a good opportunity to review the structure of your mortgage. Common examples include:

Extending the mortgage term to reduce your monthly payments

Borrowing additional funds - for home improvements, for example

Switching from a repayment mortgage to interest only (or vice versa)

Changing from a joint mortgage to a sole name, or adding a partner

These are called structural changes and require a full review of your circumstances, including affordability checks. In these cases, a client fee will apply but we'll always discuss this with you first and explain exactly what's involved before you decide.

Structural changes also mean it's especially worth comparing the whole market, as a remortgage to a new lender might open up better options alongside the changes you're looking to make.

Product Transfer vs Remortgage: Which Is Right for You?

This is the question we get asked most often by homeowners approaching the end of a fixed or tracker deal. The honest answer is: it depends on your circumstances.

If your current lender's retention rates are competitive and your circumstances haven't changed, a product transfer is often the right call. If rates elsewhere are significantly lower, or you want to change the mortgage in any way, a remortgage may be better. We'll run through both with you.

We charge no client fee for a like-for-like rate switch. For everything else, our standard advice fee, typically £495, applies.

Not sure whether a product transfer or a remortgage is the right move? Our guide to fixed vs tracker mortgages can also help if you are deciding which type of rate to take. We cover the full range of mortgage options and can talk you through the numbers at no cost.

Product Transfer Advice by Lender

Every lender handles product transfers differently. Booking windows, credit check policies, early switch options and what changes you can make alongside a rate switch all vary. We have put together detailed guides for the most common lenders our clients hold mortgages with.

Residential Mortgages

Buy to Let Mortgages

Frequently Asked Questions

What is a mortgage product transfer?

A product transfer, or rate switch, as most people call it, is when you move from your existing mortgage deal onto a new deal with the same lender, once your current one expires. Unlike a full remortgage, a product transfer does not involve switching lenders. That means no solicitor or legal fees, no full property valuation in most cases, no affordability reassessment in many cases, and a faster, simpler process from start to finish. For many homeowners, a product transfer can be the most practical and cost-efficient option but it is not automatically the right choice, which is why it is worth speaking to an adviser about your options.

Is a product transfer better than a remortgage?

It depends on your situation. A product transfer is faster and simpler, but limits you to your current lender's rates. A remortgage opens up the whole market. We can compare both options and recommend whichever works best for you.

Do Aspect Mortgages charge a fee for a product transfer?

No - we do not charge a client fee for a straightforward product transfer. A fee may apply if you want to make structural changes at the same time, such as extending the mortgage term, borrowing additional funds, or switching from repayment to interest only.

When should I start looking at my options?

We recommend reviewing your options around three to six months before your current deal ends. Many lenders allow you to reserve a new rate ahead of time, protecting you if rates rise before your deal expires.

Do I need a solicitor for a product transfer?

No. Because you are staying with the same lender and not changing the mortgage structure, there is no legal work required. This is one of the key advantages of a product transfer over a full remortgage. If you want to increase your borrowing, this becomes a structural change and a full review will be required. We will compare the best route for your circumstances, whether that is a product transfer, a remortgage, or a combination of both.

Can I increase my borrowing on a product transfer?

If you want to increase your borrowing, this becomes a structural change and a full review will be required - we will review your options and compare the best route for your circumstances. A client fee will apply in this case, but we'll always explain costs upfront.

What other mortgage services do you offer?

As well as product transfers, we advise on remortgages, first time buyer mortgages, home mover mortgages, and buy-to-let mortgages. We also have specialist advisers for self-employed applicants, contractors, and professionals. See our full range of mortgage services.

Why Choose Aspect Mortgages?

Independent and FCA regulated. We work for you, not for the lender

Whole of market access across 90+ lenders and leading insurers

Family run since 2004 with over 100 years of combined team experience

Local office, national reach. Serving clients across Lancashire, Greater Manchester and nationwide.

Real people, no jargon. Plain English, at your pace

Rated 5 stars across 470+ Google reviews. One of the most reviewed brokers in the North West

Fixed, transparent fee. One flat fee, no surprises.

What our customers say

Rated 5 stars across 470+ Google reviews, one of the most reviewed mortgage brokers in the North West.

Speak to us today

Call us on 01257 812345, or drop us a message and we will call you back

Areas We Cover

Remote advice offered nationwide.

There will be a fee for mortgage advice. The precise amount will depend upon your circumstances but we estimate that it will be £495 for a residential/buy to let mortgage or £1495 for an equity release/retirement mortgage.

Aspect Mortgages Limited is authorised and regulated by the Financial Conduct Authority and is entered on the Financial Services Register (https://register.fca.org.uk/s/) under FCA reference 305352. The FCA do not regulate Business Buy to Let Mortgages.

As independent advisers we have access to the whole market, except for deals that you can only obtain by going direct to a lender. Registered in England and Wales No: 051013801. 16 St Thomas' Road, Chorley, PR7 1HR.

A Lifetime Mortgage may reduce the value of your estate and could affect your entitlement to benefits. To understand the features and risks please ask us for a personalised illustration.

Your home may be repossessed if you do not keep up repayments on your mortgage.

© Copyright 2026 Aspect Mortgages Limited